Let us see the importance of having a Critical Illness policy and analyze which is the Best Critical illness policy in India 2020 with a comparison table.

Why we need Critical Illness Policy?

Your Life Insurance will come into picture when the insured die. Health insurance in the other hand is “Indemnity” based insurance. This means the health insurance will indemnify the cost of hospitalization. Hence, health insurance will pay you the cost of hospitalization costs.

However, in a case of critical illness policies, they are called “Fixed Benefit” plans. Assume you are diagnosed with Cancer, and then irrespective of the cost involved in treatment, an insurance company will pay you the lump sum.

Due to diagnose of critical illness, you neither may die nor hospitalized but bedridden due to this critical illness. In such a situation, along with hospitalization, you have to bear your family obligations from your own pocket.

Also, in the case of health insurance, the benefits are defined as room rent cap or ICU cap. However, in the case of critical illness insurance, an insurance company will just pay you the lump sum.

The major critical illnesses are a heart attack, cancer or a stroke. Also, there are major chances that you survive after diagnosed with such critical illness. Hence, to compensate the work loss, financial burden of kids education and your financial commitments, you need a product which can compensate such losses.

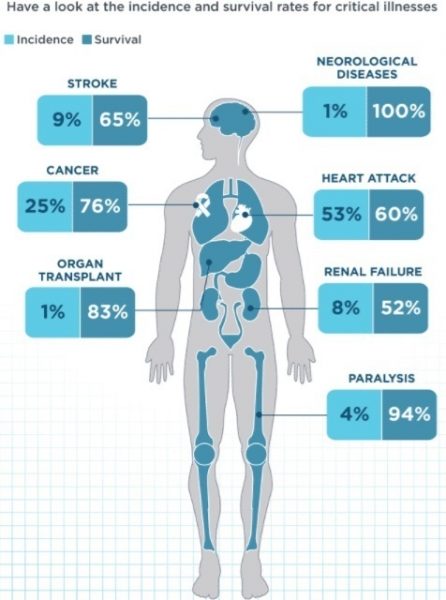

Below image will show you the possibility of survival % from the critical illness.

Source: – ICICI Lombard

Hence, we may say such survival after the critical illness will come with the COST. To compensate for this cost, you must have insurance.

No matter how good your health insurance is, there are deductibles, co-insurance payments, prescriptions that are no longer covered and exclusions. While you are recovering from critical illness, you’re not working. But that doesn’t stop the need to pay your household expenses, utility bills, EMIs towards home or car and your credit card bill.

Also, do remember that majority of health insurance products excludes the critical illness covers. Hence, it is important for you to have a critical illness.

It is not necessary for me to put some data which reflect the possibility of you and I may in future get such critical illness. Because now it is known fact that possibility is high due to our food habits, lifestyle and the stress we are into now.

Also, the medical inflation rising at an alarming rate of 10% to 12%. Hence, it is imperative for us to compensate such a high cost. We can’t pay all such costs from our own pocket. It will devastate our financial life and ruin us. Hence, it is a must for all of us to have a critical illness.

Best Critical illness policy in India 2021 -How to choose?

# Size of the cover-How much is the right cover? There is no such specific yardstick. But ideally, it should not be less than Rs.10 lakh. Also, few suggest having around 4-5 times of your annual income. But in my view, if you are capable of paying a higher premium, then go for higher cover. This will compensate for your future medical inflation for a certain year.

Ideally, I suggest the cover must not be less than Rs.10 lakh and also it must be around at least 3-4 times of your annual income.

# Illness covered-Higher the illness covered means higher the premium. Also, make sure that you must check different organs are covered than the same organs for different diseases covered. For example, a single disease may split into different cover and you may get fooled that the product is covered much critical illness.

# Definitions-The biggest task for all of us is to understand the medical terminologies. Hence, it is always best to consult a family doctor if you have doubt in this. Critical Illness policy turned to be complex for many of us because we can’t understand the medical words used in proposal or policy document.

Hence, it is a must to understand before jumping into buying.

# Sub-Limits-Insurers fix some sub-limits for each disease. For example, let us say there is a sub-limit of Rs.5 lakh for a critical illness of heart. If you diagnosed with this disease, then the insurance company will pay you Rs.5 lakh only. The policy will continue with a reduced amount of Rs.5 lakh.

# Renewal-You must always look for life long renewable products. Because the possibility of facing critical illness is high when you grow older. Hence, choose the product which offers you the life long renewability.

# Exclusion-You checks for the exclusions listed in the policy. Usually, the pre-existing diseases are covered after 3 years of the waiting period. The immediate cover of pre-existing diseases comes with a cost in higher premium. Hence, better to avoid.

Along with that, few plans specifically avoid few particular diseases. Hence, check the diseases that are excluded.

# Premium affordability-The more benefits you look for will comes with the cost. Nothing is at free. Hence, better you understand your requirement and plan accordingly. The premium will also increase as you grow older. However, if your purchased critical illness as a rider along with Life Insurance, then this will remain same throughout the policy period.

However, such riders come with limitations which sometimes may feel useless. Hence, even though standalone critical illness policies are costlier, better to go with them.

# Survival or waiting Period Clause-In critical illness policies, this is as per me is the BIGGEST drawback. Let us assume you today diagnosed with kidney failure, then these critical illness policies will accept the claim if you survived for certain period after the diagnose.

Let us assume your policy define the survival period as 30 days, then you must survive for a minimum 30 days after the first diagnoses of the critical illness. Then only you can make the claim. Assume the insured died before 30 days, then his nominee will not receive anything.

Do remember that this survival period differs for different diseases. Hence, better to check and know beforehand.

Along with that, there is a waiting period clause. It usually commences from the issue of the policy and around 90 days. Hence, an insurance company will not accept any claim if you diagnosed with a critical illness during this first 90 days of policy start.

# Claim Settlement Ratio-Even though it is hard to find the exact reasons for rejection of the claim, it gives you bit relief if you know the CSR ratio of your insurer. At the end of the day, CSR is a raw data which not point the reasons for rejection and delay in rejection. But give you some indication of how the company dealing the claims.

# Critical Illness as a RIDER or a Standalone-Many Life and Health Insurance products offer critical illness as a rider. They are cheaper than the standalone critical illness plan.

The biggest advantage of having a standalone critical illness is that the freedom to choose the coverage. Usually, in the case of Life and Health Insurance, you are not allowed to go beyond the sum assured or sum insured covered. However, in a case of standalone critical illness, you have the freedom to choose as per your comfort.

In a case of life insurance, the premium will remain same throughout the policy period. However, in a case of health insurance and critical illness insurance, it changes as you grow older (but in the case of health insurance in an age slab).

One more advantage of buying critical illness as a rider is that along with health or life insurance, your rider also gets renewed automatically when you renew both. However, in the case of standalone policies, you have to renew separately.

Nowadays few insurers offering you the disease-specific plans like Cancer Plan or Diabetic Plan. But in my view, it is better to go for plans which cover more critical illnesses than the single one or two. We don’t which critical illness we suffer.

However, when it comes to control and features, rider always comes with some restrictions. Hence, I prefer standalone critical illness.

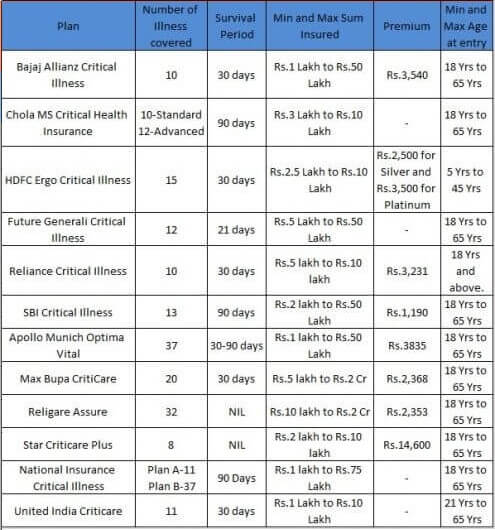

Best Critical illness policy in India 2020 – Comparative Table

Now we understood what is the importance of critical illness policy and how to choose the best critical illness policy in India. Let us now look into the available critical illness policies in India and study the comparison.

Considering the above facts, We assume HDFC ERGO, Max Bupa and Religare stands best with features and premium range and hence I consider them as “Best Critical illness policy in India”.

Income Tax Benefits of Critical Illness Insurance Policies

Premium paid by you towards critical illness insurance policies will be eligible for tax deduction under Sec.80D of IT Act. Do remember that this benefit is not available if you paid the premium through cash.

Also, any claim amount you receive from critical illness insurance policy is completely tax-free for you.

Can we buy a critical illness policy?

The critical illness policy is the complicated product which defines many medical terminologies. It is hard for a common man to understand. Also, diagnosing of critical illness not enough. Even though your doctor diagnosed it, there is no guarantee that claim will be accepted. Because the insurance company’s own doctor has to diagnose and establish that you are suffering from critical illness.

Also, the definition of diseases is not so exhaustive. Hence, there is a scope that an insurance company may reject your claim on the benefits of doubts and no clear definitions.

Check for family history of your’s for such critical illness. If you found its necessary then go ahead. Because in many cases as per insurance companies, the critical illness which they define is hard for the individual to survive. Hence, he may end up with no claim but to pay the hefty hospitalization bills.

Buy enough health insurance. If you still feel shortage, then go for super top up plans. Create an emergency fund especially for such diseases.

Hence, we feel critical illness policies are a bit complicated. Instead, I suggest enhance your health insurance and if possible go for super top-up and create an emergency fund. Rest you have to decide based on your own family history.

Conclusion:-Do remember that when you buy life insurance along with riders like Critical Illness, then you have to understand one fact that life insurance is required for a limited period. However, critical illness is required for you forever. Hence, if have a family history of critical illness, then buy the product as standalone rather than the rider.